Some topics of interest were raised in an interview with Glenn Stevens (Governor, Reserve Bank of Australia) which was published on Friday at the AFR.

The conversation on competing currencies stems from an initial question about Bitcoin (my emphasis):

The conversation on competing currencies stems from an initial question about Bitcoin (my emphasis):

Stutchbury: What do you make of Bitcoin and does that potentially have any effect on operation of monetary policy if those sort of artificial currencies or means of exchange became prevalent?

Stevens: I’m still trying to understand it to be honest but as best I can see it would be open to you to create a currency called the Michael and get people to buy it and you could promise to, you know, only issue so much of it and if people had confidence in that they could use that as a kind of numeraire. You could measure things in Michaels. You could buy and sell them.

Stutchbury: We call them “Stevens”.

Stevens: Yes. Well, and it might or might not hold its value depending on whether you keep the promise. You could also get speculative excesses in it I would imagine where its market value went up and down as people speculated on its future value and we see elements of that, I guess, with Bitcoin. I – and I think there are several other, aren’t there, similar things around so it’s a very interesting space. I don’t think it has caused us a material problem yet. I suppose it’s possible that any of these potential – these innovations financially potentially if they take off enough could – it will come back to, does it become an object of speculation with a lot of leverage behind it like a tulip mania or not. I don’t know the answer to that. I don’t know. It is certainly fascinating.

Stevens later clarifies (rightfully so) that cryptocurrencies are limited by a computer algorithm. So, unlike the initial example Stevens provides, there isn't need to worry about them holding value based on whether the issuer keeps a promise on how many will be created as it is built into the protocol.

Fiat currencies (money declared by government to be legal tender) on the other hand are not limited by an algorithm or physical backing, so are at risk of losing their value as central banks engage in various monetary policies which either directly increase the money supply or are intended to encourage borrowing which results in the same. In fact the RBA's monetary policy includes a promise to devalue the currency (with no end date):

Fiat currencies (money declared by government to be legal tender) on the other hand are not limited by an algorithm or physical backing, so are at risk of losing their value as central banks engage in various monetary policies which either directly increase the money supply or are intended to encourage borrowing which results in the same. In fact the RBA's monetary policy includes a promise to devalue the currency (with no end date):

"The Governor and the Treasurer have agreed that the appropriate target for monetary policy in Australia is to achieve an inflation rate of 2–3 per cent, on average, over the cycle." RBA

Furthermore the measure that the RBA uses as the basis of inflation is the 'Consumer Price Index' (CPI) rather than an accurate measure of the increase in Australian Dollars circulating (which are mostly borrowed into existence through private and public debt at a higher rate than the CPI).

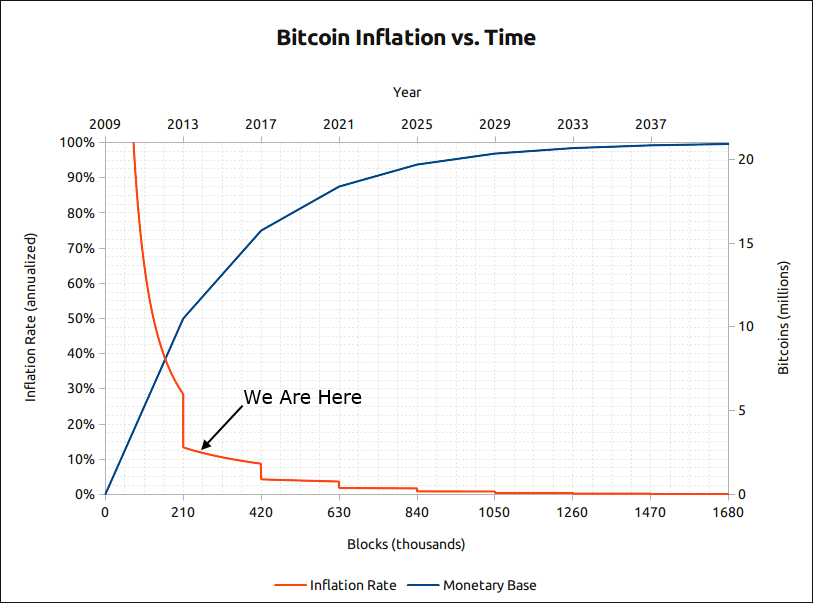

Bitcoin has an inflation rate (increase in total Bitcoins, not a cost of living index), which is currently higher than many fiat currencies. However, the rate is known in advance, it will drop over time so that within the next decade it will be lower than the RBA's measure and there will come a time when no further Bitcoins will be created.

|

| [Click Chart To Enlarge] Source |

In the response above Stevens goes on to say that cryptocurrencies may become an object of speculation 'with a lot of leverage behind it'. I would suggest there is already a lot of speculation behind the recent rise in many of their prices, but unlike traditional assets it is very difficult to do so using leverage. A bank won't lend you money to speculate on the price of Bitcoin (at least not knowingly, you may get away with using an unsecured personal loan or credit card), but they will allow you to leverage 20:1 (i.e. 95% LVR) to purchase a house. Which object of speculation using leverage is more likely to pose a risk to Australia?

In the next question the interviewer poses a question around competing currencies...

Stutchbury: Could it be that the new technology will potentially take us back to a world where there were competing currencies in any one economic system?

Stevens: Well, there are competing currencies now. I mean, you know, you can hold US dollars or Euros or whatever in Australia completely freely if you want to and there would be nothing to stop people in this country deciding to transact in some other currency in a shop if they wanted to. There’s no law against that so we do have competing currencies. Maybe – maybe there will be a world in which currencies based on some computer algorithm to limit supply as opposed to physical gold or something. There have been many such currencies through the ages. The Pacific Islands used to use shells, didn’t they? So there have been many bases for currencies and in the end, I suppose, the ones that will, and this will be a good note to finish on, the ones that survive will be the ones that hold their value which is why we have an inflation target which we’re hitting.

For starters, Australia does not allow competing currencies. The Reserve Bank Act 1959 clearly states:

Other persons not to issue notes

(1) A person shall not issue a bill or note for the payment of money payable to bearer on demand and intended for circulation.

And even prior to this Act the issuance of private notes was discouraged through the Bank Notes Tax Act of 1910 which imposed a tax of 10% per annum on all banknotes issued (by private banks).

Granted Bitcoin and other cryptocurrencies don't circulate in the form of notes, however I suspect if the creation and circulation of Bitcoin was specific to a single country then regulatory authorities would crack down on it (if they were able to, take for example the recent shutdown of physical Casascius Bitcoins in the US). It's only Bitcoin's globally distributed & digitally stored/transmitted nature that allows it to circulate outside the control of regulatory bodies.

If we ignore the fact that it's not legal to circulate private currencies and concentrate on Stevens reference to using foreign currencies in Australia, it still remains largely impractical if we are to remain within the bounds of the law. It's true that a business or individual may legally agree to transact in a currency other than the Australian Dollar:

Bitcoin is not immune from the same requirements, earlier this year the ATO commented specifically on the topic (although the comments have a business focus, it does not exempt individuals from the same requirements):

"Every sale, transaction or dealing relating to money, or involving the payment of, or a liability to pay, money in Australia is to be done in Australian currency unless it is done, or the parties to the sale, transaction or dealing agree that it will be done, in the currency of another country." RBAHowever, all parties involved are also required to report any capital gains or losses that occur as a result of foreign currency transactions. Foreign currencies are not considered a personal use asset or collectible, so fall under the title 'other assets' and are not excluded from Capital Gains Tax (CGT). Here is what the ATO has to say on foreign currency transactions:

Forex realisation event 1 occurs when there is a disposal from one entity to another (that is, a change in the beneficial ownership happens - capital gains tax (CGT event) A1 - of foreign currency, or a right or part of a right to receive foreign currency.Can you just imagine the administrative nightmare that would result from performing regular transactions in a foreign currency and having to maintain a record of whether you made a gain or loss as a result of fluctuation in the currency markets? It is simply not practical.

The time of the event is when the foreign currency, or the right or part of the right is disposed of.

You make a foreign exchange (forex) realisation gain if you dispose of foreign currency, or a right or part of a right to receive foreign currency for more than you paid for it, to the extent that the gain is due to fluctuations in the value of the foreign currency. This will usually be when the proceeds on disposal of the foreign currency, measured in Australian dollars, are more than the cost of acquiring the foreign currency, measured in Australian dollars.

You make a forex realisation loss if you dispose of foreign currency, or rights or parts of rights to foreign currency for less than you paid for them. This is to the extent that a loss is due to fluctuations in the value of the foreign currency. ATO

Bitcoin is not immune from the same requirements, earlier this year the ATO commented specifically on the topic (although the comments have a business focus, it does not exempt individuals from the same requirements):

"The tax legislation that applies to conventional commercial transactions also applies to transactions undertaken via the internet or with emerging payment systems.

Paying for goods and services with new types of payment tokens still means that the seller may need to account for GST or include the income in their business tax return.

The buyer may also need to keep records of the value of the purchase if it represents a business expense or if the purchase is an asset which may be subject to a capital gain or loss.

The value used by the buyer and the seller in these transactions needs to be identical and consistent with market prices.

It is most important that people engaged in any type of transaction with Bitcoin or other payment systems keep detailed records and evidence about what trades they make and the source of any assumptions about the value of any transaction in Australian dollars.

This will minimise the risk of there being a difference of opinion between a taxpayer and the ATO over the correct valuation and treatment of a transaction for taxation purposes." Business Insider

Ironically Stevens ends his interview on a point, 'the ones [BB: currencies] that survive will be the ones that hold their value' and in the same breath says 'which is why we have an inflation target which we’re hitting'. How Stevens equates holding value with hitting an inflation target is beyond my comprehension, it seems more like an oxymoron.

The suggestion from Stevens that we have competing currencies in Australia is, quite frankly, a joke. For true competition the laws revoking legality of private currencies need to be scrapped as do capital gains events on foreign currency transactions and for that matter Gold as I argued in an earlier post 'Let Australians Save in Gold Instead of Debt'.

The suggestion from Stevens that we have competing currencies in Australia is, quite frankly, a joke. For true competition the laws revoking legality of private currencies need to be scrapped as do capital gains events on foreign currency transactions and for that matter Gold as I argued in an earlier post 'Let Australians Save in Gold Instead of Debt'.

You can follow me on Twitter. I'm usually sharing links and opinions daily (@BullionBaron). You can also CLICK HERE to signup for free email updates.

BB.