A hundred years ago, in 1913, the first Australian currency note (10 Shillings) was issued (as a blue banknote). Payable in Gold, the note was equal to a half sovereign gold coin (3.99g of 22k Gold, roughly A$165 spot value today). Australia formally departed from the Gold standard during the great depression in the early 1930s when the Commonwealth Bank Act of 1932 made Australian currency notes no longer convertible into Gold. In 1931 the Australian currency was pegged to the British Pound, in the 1970s it was pegged to the US Dollar, followed by a basket of trade weighted currencies before being floated in 1983.

Today the Australian dollar is not redeemable for Gold, it is not pegged at a fixed exchange rate against other currencies and the number created doesn't have a fixed limit (a la Bitcoin), today most Australian dollars are borrowed into existence.

I have seen it suggested that a bank must receive a deposit from which it can then lend a majority portion. In fact when someone borrows money from a bank, the bank can create new money (or credit) out of thin air. It will credit the borrower with a deposit (which might be paid in form of a cheque or deposit into the borrowers account) and will also create a loan account for which the bank charges interest on the created money (this is an asset for the bank, earning it income).

When a bank lends money, the deposit ends up in the hands of the borrower without anybody else having less, hence we have just seen an increase in the total money available. In today's monetary system 'money is debt', it is backed by the ability of borrowers to repay their loans, that is something that should strike fear into the hearts of savers given the reckless abandon with which banks lend today.

Australian dollars can be borrowed into existence by the government running a deficit (borrowing to spend more than it receives in revenue) or via the private sector. Government debt today is relatively low, but has been on the rise since the GFC:

Today the Australian dollar is not redeemable for Gold, it is not pegged at a fixed exchange rate against other currencies and the number created doesn't have a fixed limit (a la Bitcoin), today most Australian dollars are borrowed into existence.

I have seen it suggested that a bank must receive a deposit from which it can then lend a majority portion. In fact when someone borrows money from a bank, the bank can create new money (or credit) out of thin air. It will credit the borrower with a deposit (which might be paid in form of a cheque or deposit into the borrowers account) and will also create a loan account for which the bank charges interest on the created money (this is an asset for the bank, earning it income).

When a bank lends money, the deposit ends up in the hands of the borrower without anybody else having less, hence we have just seen an increase in the total money available. In today's monetary system 'money is debt', it is backed by the ability of borrowers to repay their loans, that is something that should strike fear into the hearts of savers given the reckless abandon with which banks lend today.

Australian dollars can be borrowed into existence by the government running a deficit (borrowing to spend more than it receives in revenue) or via the private sector. Government debt today is relatively low, but has been on the rise since the GFC:

Increases in the government debt to GDP ratio are typically due to two occurrences: world wars (1914 to 1918 and 1939 to 1945) and responses to economic downturns caused by private debt-financed speculation: the 1890s, 1930s, mid-1970s, early 1980s, early 1990s and the GFC in 2008. The rise in the ratio before the 1890s was due to colonial government mass construction of public infrastructure. Philip Soos, Prosper

As can be seen in the above chart, private debt has been a much larger contributor to money growth over the last 40 years. Private sector debt includes household borrowing (primarily for mortgages), investment & business loans amongst other sources.

With private debt having increased at an alarming rate over the last two decades to levels not yet seen in Australia's history (relative to GDP) it should be no surprise that the government and banks are making preparations to socialise the losses across all bank depositors, should the need ever arise.

With private debt having increased at an alarming rate over the last two decades to levels not yet seen in Australia's history (relative to GDP) it should be no surprise that the government and banks are making preparations to socialise the losses across all bank depositors, should the need ever arise.

It's not hard to work out where most of the money created by the private sector has flowed...

By any measure Australian land valuations are at nose bleed levels relative to historical norms using several measures, with The Economist indicating our house prices are overvalued 46% relative to rents and 24% relative to incomes:

So where does this massive push of money (debt) into land values leave savers?

Many savers probably point to an increasing bank balance every year and think that their savings are growing, but if we look at real returns after inflation and tax, even the official story shows they are lucky to be breaking even:

That wouldn't be so bad (breaking even, maintaining purchasing power with the money they put aside for spending later), that is if CPI was an accurate measure of the rate at which their purchasing power was declining. For those intending to save money and purchase property in the future, their purchasing power has been eroded more significantly. The removal of land costs for owner-occupiers from the CPI in 1998 assists with hiding the loss of purchasing power in the above chart:

The resulting MacroStats cost-of-living index is plotted below against the headline CPI... We can again see how this measure tracks the official CPI very closely until 1998. Since 1998 it is 0.73 percentage points higher on average (or 3.8%), and in the period 2001-2008, it averaged 1.3 percentage points higher (or 4.4%pa). That gives you some idea of how significant the 1998 methodological shift in the CPI was in disguising housing inflation and creating a feedback loop with lower monetary policy. Rumplestatskin, MacroBusinessTo measure loss of purchasing power you really need to have a look at how the value of your savings has performed relative to what you intended to purchase with those savings. Those saving in Australian dollars over the last 15 years, with the intention to purchase property, have been severely disadvantaged by the drop in their purchasing power.

Money is primarily understood as a unit of account, a store of value and a medium of exchange, but there doesn't necessarily need to be one monetary asset to perform all these roles. The below is an extract from a Freegold blog called 'Flow of Value':

Which tool is best for which job is a subjective decision, best left to the sovereign entity (whether individual or state) evaluating their own money. The criteria used in making this subjective assessment may be infinite, but the most important of these is time: how long does one anticipate holding this money? If the answer is short term (ie. "spending money", used for current expenses), then the best form to hold it in is a fiat currency. If the answer is longer term (ie. "savings", a surplus over and above what is required as shorter term "spending money"), then the best form is gold, to protect ones buying power.In my opinion individuals should have a choice in what money/currency they choose to save in (and/or transact with).

In

the United States some libertarians have proposed to allow

Gold & Silver to act as a 'competing currency' to fiat, as explained

in this bill (H.R. 4248 (111th): Free Competition in Currency Act of 2009):

Free Competition in Currency Act of 2009 - Repeals the federal law establishing U.S. coins, currency, and reserve notes as legal tender for all debts, public charges, taxes, and dues. Prohibits any tax on any coin, medal, token, or gold, silver, platinum, palladium, or rhodium bullion issued by a state, the United States, a foreign government, or any other person. Prohibits states from assessing any tax or fee on any currency or other monetary instrument that is used in interstate or foreign commerce and that has legal tender status under the Constitution. Repeals provisions of the federal criminal code relating to uttering coins of gold, silver, or other metal for use as current money and making or possessing likenesses of such coins. Abates any current prosecution under such provisions and nullifies any previous convictions.

What attributes make Gold the best monetary asset to free up for individuals use to protect purchasing power? Jordan Eliseo touches on one of the most important in a recent market update:

Apart from the critique about its lack of yield, the second most commonly heard objection to investing in gold, or valuing gold at all, is that it has ‘no use’.

But what does this criticism really mean? Certainly it is accurate that gold has no (or at least minimal) industrial use. But it is an incomplete observation, for whilst gold ‘lacks use’ from the standpoint of a traditional commodity, this ‘drawback’ is of course precisely gold’s virtue.

Any commodity that did have an industrial use (and was the refore consumable), would by nature suffer from an uncertain overall supply, making it unfit as a monetary asset as unarguably the most important pre-condition for good money is stability.

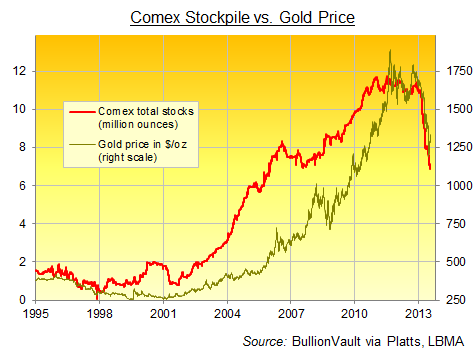

The short term price of Gold is dictated on an exchange where paper based contracts trade in place of physical metal, so price stability is not something afforded to Gold in the present climate. However, Gold does offer long term stability in price as shown by consistently returning to similar valuations relative to goods and other asset classes (including, but not limited to house prices, oil & stocks).

Another way Gold offers stability is in it's new supply, in fact the low increase in overall supply each year has resulted in a remarkably stable amount of Gold per capita over the last century (as previously covered on the blog):

Another way Gold offers stability is in it's new supply, in fact the low increase in overall supply each year has resulted in a remarkably stable amount of Gold per capita over the last century (as previously covered on the blog):

1900: 1.65 billion people / 1.54 billion ounces = 0.935 oz Gold per capita

2010: 6.97 billion people / 5.46 billion ounces = 0.783 oz Gold per capita

2010: 6.97 billion people / 5.46 billion ounces = 0.783 oz Gold per capita

One of the main barriers holding back people from having the freedom to use Gold as money today (either as a store of value, medium of exchange or both) is the crippling paperwork and gains/losses that would arise in the current environment, Keith Weiner expanded on this in a recent article (US centric, but same principal applies in Australia):

The capital gains tax renders it inconvenient to use gold and silver as currency.

We should repeal the capital gains tax on gold and silver. If the paper dollar serves our modern economy better than gold then people will continue to choose it. Most economists, notably Nobel Prize winner Paul Krugman, are opposed to any form of gold standard. They think that a purely paper money is good for us, and that gold won’t work. However even without coercive laws, people choose cars over horses and mobile phones over telegraphs. There is no need to force people to do what’s good for them.

So most economists have it backwards. It is the fiat dollar that does not suit a modern free market economy. People will migrate toward gold and silver when we remove the artificial barriers. This experiment will solve the mystery, and liberate people to hold and spend their money as they choose.

Capital gains tax (and in some cases GST) would make it near impossible for Australians to use Gold (and/or other precious metals) as a competing currency. Purpose should play a part in whether an asset is taxed. Consider the following scenarios...

First scenario: A family buys a $300k property in Suburb A, prices rise to $400k and they want to move to Suburb B which is also $400k and risen by the same amount. Should they have to pay tax on the $100k profit (when they sell the first house to buy the next) even though they are not better as a result (and in fact will be worse off only due to moving suburbs)?

Second scenario: A business man intends on buying an $800 laptop from overseas. While saving to purchase the laptop the Australian dollar plunges in value and as a result he is able to purchase the laptop for $80 less, should he have to pay tax on this material gain? What about if the Australian dollar had strengthened and he had to pay $80 more, should he be able to claim that as a capital loss or tax deduction?

Third scenario: A family is saving for a home in Australian dollars from 1998 to 2013, their purchasing power in order to buy a home has been decimated due to prices rising well above the level of official inflation and the after tax return on their savings. Once they have purchased the home should they be able to claim the purchasing power they've lost as a deduction/capital loss?

Fourth scenario: A family is saving in Gold (with intent to purchase a home) from 2005 to 2013 and as a result of doing so their purchasing power has increased due to a strong gain in Gold relative to house prices. Should they have to pay tax on the gain when they sell their Gold to buy the house?

Hopefully you can see the point I am trying to make. Tax isn't always appropriate, especially in a situation where people are using Gold (or another currency for that matter) as a medium of exchange or savings vehicle.

Give Australians a choice, let us save in Gold instead of debt.

---------------------------------------------

At the start of the year I posed a suggestion to the Liberal Democratic Party (forum link, requires registration to view) that they consider a precious metals policy to attract a group of voters who are disenchanted with Australia's political landscape and have a mostly libertarian philosophy. The suggestion was initially met with positive feedback:

So the above post aimed to bring some focus to to the reasons it might be a

good idea to allow Gold to act as a competing currency to the Australian

dollar.

The core policies I would like to see a political party adopt in order to enable the above (and to tidy up some other precious metals related inconsistencies):

First scenario: A family buys a $300k property in Suburb A, prices rise to $400k and they want to move to Suburb B which is also $400k and risen by the same amount. Should they have to pay tax on the $100k profit (when they sell the first house to buy the next) even though they are not better as a result (and in fact will be worse off only due to moving suburbs)?

Second scenario: A business man intends on buying an $800 laptop from overseas. While saving to purchase the laptop the Australian dollar plunges in value and as a result he is able to purchase the laptop for $80 less, should he have to pay tax on this material gain? What about if the Australian dollar had strengthened and he had to pay $80 more, should he be able to claim that as a capital loss or tax deduction?

Third scenario: A family is saving for a home in Australian dollars from 1998 to 2013, their purchasing power in order to buy a home has been decimated due to prices rising well above the level of official inflation and the after tax return on their savings. Once they have purchased the home should they be able to claim the purchasing power they've lost as a deduction/capital loss?

Fourth scenario: A family is saving in Gold (with intent to purchase a home) from 2005 to 2013 and as a result of doing so their purchasing power has increased due to a strong gain in Gold relative to house prices. Should they have to pay tax on the gain when they sell their Gold to buy the house?

Hopefully you can see the point I am trying to make. Tax isn't always appropriate, especially in a situation where people are using Gold (or another currency for that matter) as a medium of exchange or savings vehicle.

Give Australians a choice, let us save in Gold instead of debt.

---------------------------------------------

At the start of the year I posed a suggestion to the Liberal Democratic Party (forum link, requires registration to view) that they consider a precious metals policy to attract a group of voters who are disenchanted with Australia's political landscape and have a mostly libertarian philosophy. The suggestion was initially met with positive feedback:

"The LDP is always interested in attracting new members / voters to its platform, so any policy idea that achieves that aim and accords with our principles would be welcome.

I'll need to educate myself on the subject before I can add to your discussion, but your thread is definitely not pointless and I hope we can develop a meaningful policy that meets the aims stated in your original post."

However,

after spending several hours collaborating with the Australian precious

metals community, writing a policy and then clearing up some finer

points with questions posed on the LDP forum I was provided the

following disappointing response (from another senior member of the

site/party):

"What you are arguing is a variation of a return to a gold standard. There are plenty in the party who agree with that, and also advocate an end to fiat currency.

We have discussed whether we should do anything about it in policy terms. The conclusion is that there are no votes to be won and the major parties would not pinch the policy, so it's not really worth the trouble.

The only way I can see it gaining acceptance is if you made it very easy to understand and implement. Consider also how our members would explain it to their friends."

The core policies I would like to see a political party adopt in order to enable the above (and to tidy up some other precious metals related inconsistencies):

1. Repatriate Australia's Gold Reserves (99.9% are held overseas at the Bank of England).

Australia's Gold is stored with the Bank of England (as previously discussed on this blog). With only 1 tonne (of 80) on loan there seems little point leaving the Gold on foreign soil. Bringing it back to Australia would also act as a deterrent to the Reserve Bank of Australia (RBA) selling our Gold, a move which would not surprise given light of recent comments from the RBA's Assistant Governor, Guy Debelle: “If you think about the intrinsic value of gold, there’s not a lot. Gold often has a high price because people believe that other people believe that it’s worth a lot. When you describe other markets like that, the word ‘bubble’ gets thrown about.”

2. Increase the scope of the

definitions "precious metal" & "investment grade bullion" (for

taxation purposes) to include all four precious metals in the ISO 4217

currency code standard.

There are four precious metals with a currency code; Gold (XAU), Silver (XAG), Platinum (XPT) & Palladium (XPD). The first three are specifically defined for taxation purposes in Australia as "investment grade bullion" (providing they meet required finesse). Palladium is not listed, however wording in Australian tax law leaves the potential for Palladium to be included: "Any other substance (in an investment form) specified in the regulations of a particular fineness specified in the regulations." This change would specifically add Palladium to the definition of "investment grade bullion" for taxation purposes (aligning it with the other three precious metals) for uniformity.

3. Increase the scope of the

definitions "precious metal" & "investment grade bullion" for

taxation purposes to include coins containing Gold, Silver, Platinum or Palladium (any

finesse) which are now or once were legal tender of Australia or any

other nation and which trade as a function of the spot price.

Precious metals are often traded in widely recognised investment forms which don't meet the strict scope defined by the Australian Taxation Office. Investment grade bullion below 99% for Platinum, 99.5% for Gold and 99.9% for Silver is subject to Goods and Services Tax (GST). This means dealers are required to charge GST on coins which many hold for investment purposes, but aren't exempt from GST, for example American Gold Eagles (91.6% Gold), Gold Sovereigns (91.6% Gold) and Round Australian 1966 50 Cent Pieces (80% Silver). Such legal tender coins which trade as a function of spot price (consistently trade at spot + x% premium) would be made exempt from GST.

4. Repeal Part IV (currently suspended) of the BANKING ACT 1959 which

allows for the confiscation of Gold from Australian citizens by

requiring them to return personal Gold Holdings to the Reserve Bank of

Australia at a price set by the Reserve Bank.

While this section in the Banking Act 1959 has been suspended since 1976, there are provisions in Part IV to confiscate Gold from Australian citizens (as described in detail here by Bron Suchecki). Even though suspended, repealing this part of the Banking Act would be a show of good will that the government has no intention of confiscating the Gold of Australian citizens in the future.

5.

Introduce an exemption for Capital Gains Tax on "precious metal" &

"investment grade bullion" and securities fully backed by investment

grade bullion.

Where an individual is using Gold (or any other investment grade bullion) as a savings vehicle or medium of exchange, no capital gains tax would be applicable.

---------------------------------------------

You can follow me on Twitter. I'm usually sharing links and opinions daily (@BullionBaron). You can also CLICK HERE to signup for free email updates.

BB.

-for-Jul-2013.png)